OfNE SCENE China’s coronavirus recovery has caught the world’s attention more than ever: a huge pool party in Wuhan in August, the city where the epidemic began. About four months after their 11-week lockout, the revealers were huddled together in waist-high water, jumping and screaming for joy. DJ Bass-heavy heartbeat cut. The video went viral. It was a moment of redemption and an indication of how far China is ahead of other countries in returning to normalcy. Economic figures are hardly as enthusiastic as the pool parties, but China’s latest GDP The figures released on October 19 were equivalent to those of Wuhan’s ships.

Officials said the economy grew 4.9% in the third quarter compared to a year earlier, a shame ahead of the epidemic. While many other countries are mired in recession and are grappling with a new wave of Covid-19 cases, China has only completed one upper part. Also-Your counterattack. As an analyst, its success is easy to explain. China got one important thing right. Almost expelling the virus, it was able to resume activity with some restrictions. Schools are fully open, factories are booming and restaurants are booming. China is also fortunate in a significant way. This is better than weaker global demand than smaller partners like New Zealand, which has done a better job of preventing the epidemic. Until the vaccines are introduced, others will continue to struggle to accomplish China’s feat.

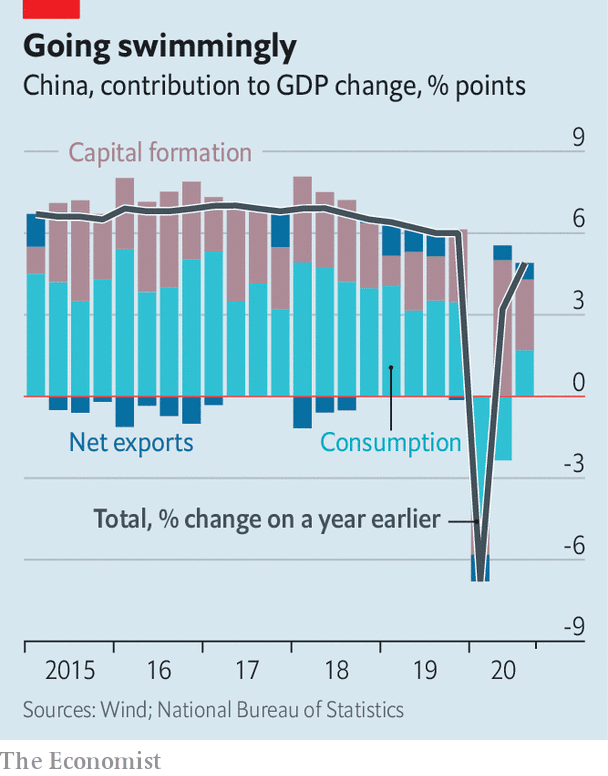

Yet China’s headline resilience has masked an unbalanced recovery. In February, when the government began working cautiously to ease its lockout, it focused on reopening factories and resuming infrastructure projects. It reasoned that maintaining strict health protocols in factories and construction sites, which could be maintained as a semi-closed environment, would be easier than shopping malls or schools. On top of that, China’s mediocre arrangements for unemployment insurance meant that millions of people found themselves out of work, having to cut back on their expenses. Early in its recovery, China’s economy was thus stimulated by factory production and investment. Capital formation in category GDP The accounting that accompanies these efforts contributed five percentage points to growth in the second quarter, while consumption declined by more than two percentage points. At that time, China left with a 3.2% year-on-year growth rate.

The latest data shows a slightly more balanced recovery (see chart). Contributions to third-quarter growth from capital formation fell by less than three percent, according to epidemiological precedents, as basic spending cuts off. Consumption added about two percentage points below its pre-epidemic height but a big improvement – easily visible in crowds returning to tourist spots, restaurants and shops. The trade was cream on top. China’s share of global trade exports has reached record highs during the epidemic. It was boosted by being the first manufacturing force to resume operations, from being the world’s largest manufacturer of protective equipment ranging from masks to surgical instruments.

Whenever Chinese data looks so complex, it is natural to ask whether they are reliable or not. In this case non-GDP Indicators lend a strong bearish picture, including exports to China by other countries. The biggest concern is whether the recovery has been at the expense of debt control efforts. Government-led rise in bank lending after initial economic downturn will put pressure on China’s debtGDP This year the ratio is about 275%, higher than 25 percentage points. This will be the largest annual increase since 2009 during the global financial crisis.

Yet China is far from alone. Governments around the world have run big tabs to mitigate the economic downturn from the epidemic. With its growth on the way, China has a chance to plant spigots again. S.&P, A credit-rating agency, notes that the country’s real lending rates (ie adjusted for inflation) have recently climbed to a five-year high, which is a dampener for investment. If successful, China will limit irrational excitement in the ponds. ■

This article is published in the China section of the print edition under the heading “A Big Break”

Cory Weinberg is a contributor to Sproutwired.com, covering a wide range of topics including news, politics, business, technology, sport, entertainment and lifestyle. He focuses on delivering clear, balanced reporting that helps readers stay informed about current events and emerging developments. Cory’s work highlights relevant stories, practical insights and important issues affecting communities and industries, with an emphasis on accuracy, clarity and information that readers can trust.