In Monday’s early buying and selling, Tesla’s current market capitalisation is touching a mammoth $320bn. It’s been very a operate for the electrical vehicle corporation considering that March, when its shares briefly fell underneath $400 at the top of the coronavirus stress. At the time of writing, they are $1,744. People brave enough to acquire the dip have been duly rewarded.

Tesla’s valuation is even more eye-watering than it was when we last looked at the company again at the conclusion of April, and while there’s been optimistic information, not the very least from second-quarter deliveries, it is difficult to see how it justifies an further $180bn in market capitalisation.

Though its temping to place the price moves down to working day traders, algos or delta-hedging, it’s tough to truly know what’s pushed the company’s valuation to 13 moments Ford’s.

But rate motion, in and of itself, has a way of generating its individual justifications for a enterprise. And so it is been with Tesla.

A well known narrative we’ve found ex-ante from bulls of late, these types of as CNBC’s Jim Cramer or Harvard Organization Review, is what we like to refer to as “the Amazon fallacy”.

You know the argument. Amazon, for the most aspect, sustained losses in its early daily life as it focused on scale and industry share in on the web retail. Thanks to this, Bezos was in a position to develop a company leviathan with a stranglehold across voice-activated speakers, cloud infrastructure and cardboard waste generation. Tesla, or any other lossmaking company with a imprecise tech angle which is an investor darling, is hence the perhaps exact.

There are several concerns with this argument. Ex-Alphavillain Kadhim Shubber picked around a person again in 2017, when a couple United kingdom-primarily based venture capitalists tried to protect money-incinerating food items delivery business enterprise Deliveroo’s negative gross margins.

For Tesla, having said that, the real level of change with Amazon boils down to hard cash move.

“Revenues are vanity, profit are sanity but money is reality” is a well-liked axiom in the organization globe, and for superior explanation: dollars stream allows enterprise operations to be sustained devoid of the kindness of strangers, or diluting current investors.

Bezos, when he started Amazon, realized this. In his famed 1997 letter to shareholders, the very first posted just after the enterprise went community, he stated that when presented with the alternative, he would eschew profitability for “maximising the current price of upcoming money flows”:

Later on in his 2004 letter to shareholders, potentially in response to worries more than Amazon’s profitability, Bezos expanded on this issue:

Our final fiscal measure, and the just one we most want to drive above the extended-phrase, is cost-free hard cash stream per share.

Why not concentration initially and foremost, as quite a few do, on earnings, earnings for each share or earnings development? The simple response is that earnings never instantly translate into cash flows, and shares are value only the existing worth of their long run dollars flows, not the current price of their long run earnings. Long term earnings are a part — but not the only critical element — of upcoming hard cash move per share. Doing work capital and cash expenses are also crucial, as is long run share dilution.

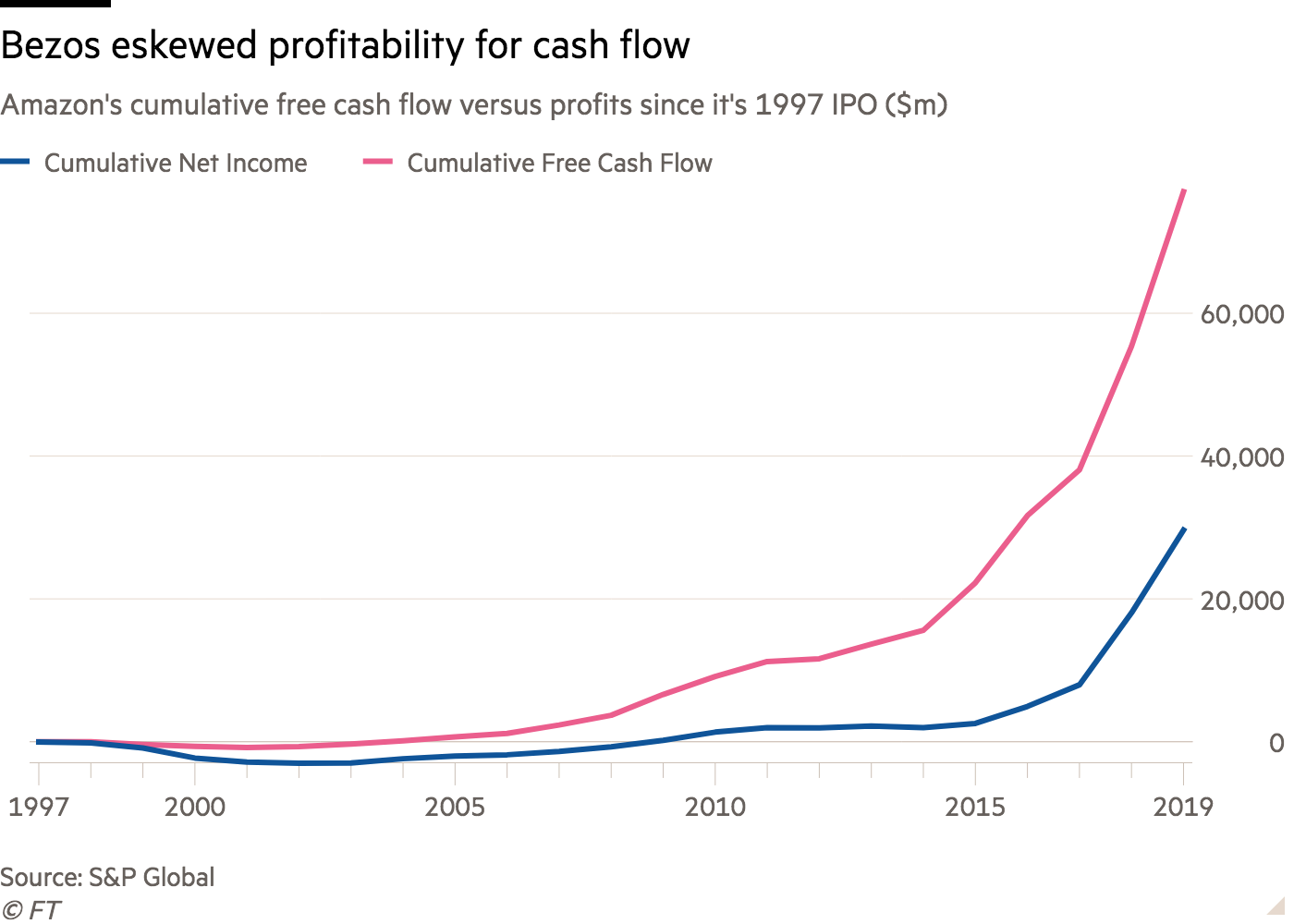

And he’s delivered. Here’s how Amazon’s cumulative cost-free cash movement (calculated as running money movement minus funds expenditure) appears vs . its profitability considering the fact that it IPO’d again in 1997:

More than this 23-calendar year time period, Amazon has created 2.6 occasions as much no cost income stream as income.

This has meant it’s been in a position to fund its new business lines — from successes like Amazon Net Companies to failures like the Fireplace Mobile phone — without having frequently returning to the sector with cap in hand. To that position, include up Amazon’s dollars movement from financing in excess of the many years, and you’ll find the harmony is negative — ie, it is returned a lot more money to buyers than it’s extracted from the marketplace (mostly in the kind of debt repayments).

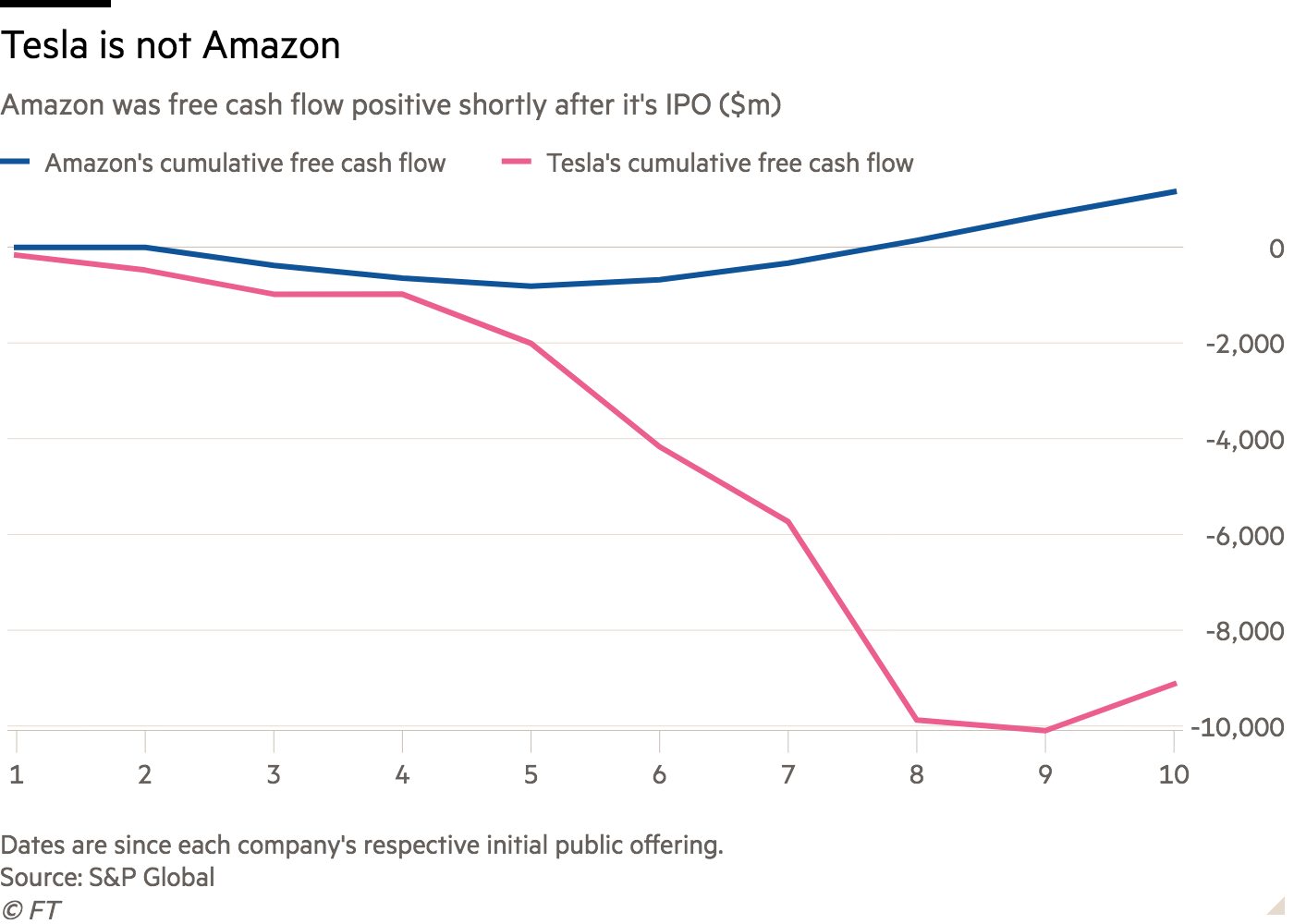

Tesla could not be a lot more diverse. The easiest way to reveal this is to compare the two providers in excess of the historic intervals due to the fact their original public choices in 1997 (Amazon) and 2010 (Tesla) respectively.

Both seasoned fast earnings development as their operations expanded but when it will come to free money flow, it is chalk and cheese:

There are various causes for this, but the most obvious one is that Tesla, fundamentally, is a motor vehicle company. To equally sustain and grow operations, automakers call for continuous reinvestment in the sort of money expenditure.

And that’s what would make Amazon incomparable, simply because even nevertheless its warehousing and logistics also needed further cash, it was able to leverage its associations with suppliers to produce dollars, by shelling out them slower than the time taken to acquire hard cash from its consumers.

If Tesla does handle to defy the sceptics and sustain its dominant posture in electric powered autos — which is significantly from apparent — it won’t glance something like Amazon’s route to the all-conquering company it is nowadays.

On the other hand, there is also one more level to be produced below, and it applies to the broader investor enthusiasm we have witnessed for companies with significant whole addressable markets — no matter whether it be in the software-as-a-services, electrical automobile or quasi-transportation sector — over the previous couple of months.

Throughout the dotcom boom, Amazon’s prospective clients as the chief in ecommerce experienced traders salivating and they rewarded the corporation by bidding its valuation up to a $25bn by the finish of 1999 — around 25 moments revenues.

They were proper. Amazon did turn into the sector leader, and not just in e-commerce. But, in the quick time period, becoming directionally suitable was not rewarded by the industry.

Amongst December 1999 and September 2001, Amazon’s shares fell 94 for each cent, as the dotcom growth turned to bust.

Tech buyers hoping a organization may possibly turn out to be the upcoming Amazon — irrespective of no matter if the comparison is legitimate or not — must just take take note.

Linked Back links:

Is Deliveroo an ‘Amazon’? — FT Alphaville

Henry Lawson is a contributor at Sproutwired.com, covering a wide range of topics including news, politics, business, technology, sport, entertainment and lifestyle. He focuses on delivering clear, accurate and reader-friendly reporting that helps audiences stay informed about current affairs and important developments. With an emphasis on useful information and balanced coverage, Henry aims to highlight stories that matter most to readers, providing context and insight in a straightforward and accessible way.